This article originally appeared in First Mover, CoinDesk’s daily newsletter putting the latest moves in crypto markets in context. Subscribe to get it in your inbox every day.

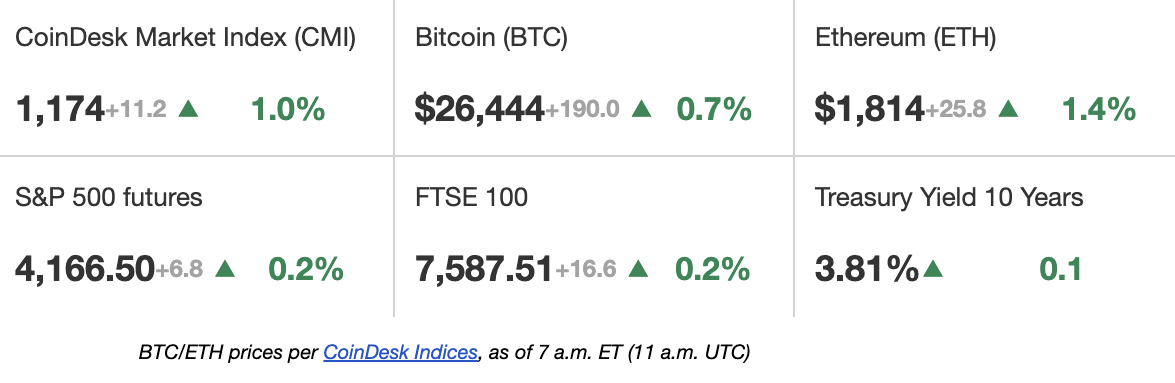

Latest Prices

Top Stories

Digital Currency Group (DCG), the parent company of CoinDesk is closing down its trade execution and prime brokerage services unit, TradeBlock, citing crypto winter and regulatory uncertainties. The shutdown of the unit, which provides trading services to institutional investors, will be effective as of May 31, a DCG spokesperson told CoinDesk. TradeBlock was acquired in 2020 by CoinDesk, and was later spun out as its own standalone business. CoinDesk kept the index data operating from the deal, which was rebranded as CoinDesk Indices, and “has proven to be a successful acquisition,” the spokesperson said. The story was first reported by Bloomberg.

The number of ether (ETH) on exchanges has hit a low not seen since July 2016 as staking saps up available tokens. Data from Glassnode shows that as of Thursday, 14.85% of all ether was held in wallets owned by centralized exchanges. That’s the smallest proportion since ether was in its infancy during the summer of 2016. In contrast, during the bull market of 2021, the exchange balance was around 25%. Low exchange balances are typically thought to be a bullish sign as it means the supply of ether available for purchase is limited.

U.S. Bitcoin Corp. (USBTC) is set to become one of the largest miners in America following a deal to buy mining assets from bankrupt lender Celsius. The company is part of the Farenheit consortium that won a bankruptcy auction for the Celsius assets, which include a lending portfolio, cryptocurrencies and 121,800 mining machines. Once it brings all the mining rigs online, its fleet will total at least 270,000 mining rigs and computing power of 12.2.exahash/second (EH/s), the firm told CoinDesk, putting U.S. Bitcoin Corp. alongside other U.S. mining giants likes Riot Platforms (RIOT), Core Scientific (CORZ) and Marathon Digital Holdings (MARA).